MQL Articles is a repository that contains the basic structure of the complete framework by Leo\Nique_372 (TradeSystemsNique - TSN), in addition to containing the codes that nique_372 implemented in his MQL5 articles (Ict, Risk Management, Position Management).

- MQL5 92.6%

- MQL4 7.4%

| Defines | ||

| Examples | ||

| Images | ||

| IndicatorsCts | ||

| Ob | ||

| PosMgmt | ||

| RM | ||

| Sets/Article_19682 | ||

| Strategy | ||

| Utils | ||

| CHANGELOG.md | ||

| dependencies.json | ||

| LICENSE | ||

| MQLArticles.mqproj | ||

| README.md | ||

A comprehensive collection of MQL5 implementations for risk management and position management in algorithmic trading. This repository contains the source code from articles published on MQL5.com by nique_372..

Main features

RM

Oco order

COcoOrder oco;

void Function()

{

.

.

unsigned long ticket1 = trade.ResultOrder();

.

.

unsigned long ticket2 = trade.ResultOrder();

oco.AddOrders(ticket1,ticket2);

}

Risk management

CRiskManagement rm;

// Note: "rm" requires that the lot, type, maximum profit and loss be reset, etc., before calling functions like CalculateSL, GetLote, etc.

// Check superated

if(g_loss_profit_manager.MaxLossIsSuperated())

{

risk.CloseAllPositions();

CanTrade = false;

}

// Calcule lot size

double entry_price = 1000.0;

double l = risk.GetLote(ORDER_TYPE_BUY, entry_price, 100, 0);

// Calcule SL

long sl = risk.GetSL(ORDER_TYPE_BUY, entry_price, 100, 0)

// And more (GetPositionsTotal, SetStopLoss, CloseAllOrders, GetPositions, etc..)

Strategy

Basic configuration

CAtrUltraOptimized* atr_ultra = new CAtrUltraOptimized();

atr_ultra.SetVariables(PERIOD_CURRENT, _Symbol, 0, 14);

atr_ultra.SetInternalPointer();

strategy.AddLogFlags(InpStrategyLogLevel); // Log Flags

strategy.SetAtrTP_SL(atr_ultra, INP_STRATEGY_ATR_MULTIPLIER_TP, INP_STRATEGY_ATR_MULTIPLIER_SL); // TP sl by atr

strategy.SetOperateMode(TR_BUY_SELL, INP_STRATEGY_TYPE_TPSL); // Operate mode

strategy.SetTP_SL(INP_STRATEGY_SL_POINT, INP_STRATEGY_TP_POINT); // TP SL by point

if(InpRmLoteType == Fijo)

strategy.FixedLotSize(InpRmLote); // Fixed lot size

Filters

// Filter RSI

if(INP_FILTER_RSI_ENABLE)

{

CSFilterRsi* f = new CSFilterRsi();

strategy.AddFilter(f);

}

// Filter Stochastic

if(INP_FILTER_STOCH_ENABLE)

{

CSFilterStochastic* f = new CSFilterStochastic();

strategy.AddFilter(f);

}

// Filter Bollinger Bands

if(INP_FILTER_BANDS_ENABLE)

{

CSFilterBands* f = new CSFilterBands();

strategy.AddFilter(f);

}

// Codigo

g_strategy_filter_general_parser.AddLogFlags(InpFIlterLogLevel);

strategy.CodeCompra<CStrategyFilterEmptyFuncFac>(StringFormat("#group oAnd (%s,%s,%s,%s,%s,%s,%s) == 0 oAnd ([%s] == 0 oOr [%s] == 2)",

CSFIlterAD_NAME, CSFilterSuperTrend_NAME, CSFilterFvg_NAME, CSFilterBands_NAME, CSFilterRsi_NAME, CSFilterStochastic_NAME, CSFilterLiqEstimed_NAME, CMediationsByZoneFilterName, CMediationsByZoneFilterName), 5);

strategy.CodeVenta<CStrategyFilterEmptyFuncFac>(StringFormat("#group oAnd (%s,%s,%s,%s,%s,%s,%s) == 1 oAnd ([%s] == 1 oOr [%s] == 2)",

CSFIlterAD_NAME, CSFilterSuperTrend_NAME, CSFilterFvg_NAME, CSFilterBands_NAME, CSFilterRsi_NAME, CSFilterStochastic_NAME, CSFilterLiqEstimed_NAME, CMediationsByZoneFilterName, CMediationsByZoneFilterName), 5);

// Summary

strategy.PrintFilters();

Position management

Breakeven

//--- Atr

atr_ultra_optimized.SetVariables(_Period, _Symbol, 0, 14);

atr_ultra_optimized.SetInternalPointer();

//--- We set the breakeven values so its use is allowed

break_even.SetBeByAtr(InpBeAtrMultiplier, InpBeAtrMultiplierExtra, GetPointer(atr_ultra_optimized));

break_even.SetBeByFixedPoints(InpBeFixedPointsToPutBe, InpBeFixedPointsExtra);

break_even.SetBeByRR(InpBeRrDbl, InpBeTypeExtraRr, InpBeExtraPointsRrOrAtrMultiplier, GetPointer(atr_ultra_optimized));

break_even.SetInternalPointer(InpTypeBreakEven);

break_even.obj.AddLogFlags(InpLogLevelBe);

Partial closures

g_partials.AddLogFlags(InpLogLevelPartials);

g_partials.Init(InpMagic, _Symbol, InpVolumenQueSeQuitaraDeLaPosicionEnPorcentaje, InpPartesDelTpDondeSeTomaraParciales);

Conditional partial closures

if(InpPartialsIsEnable)

{

// Atr creation

g_atr = new CAtr();

g_atr.Create(_Period, _Symbol, 14, true, true);

g_atr.SetAsSeries(true);

CAutoCleaner::AddPtr(g_atr); // Añadimos para que se auto elimine

// We assign to g_partilas the dynamic instance returned by CConditionalPartialsFactory::Create(...)

g_partials = CConditionalPartialsFactory::Create(InpPartialsClassManagerType); // Sera elimnado globalmente

// Initial log flags

g_partials.AddLogFlags(InpPartialsLogLevel);

// Create condition

CConditionalPartialsIndRsi* rsi_condition = new CConditionalPartialsIndRsi(); // True dado que sera eliminado por partials

// Rsi condition config

if(!rsi_condition.Init(InpPartialsRsiTimeframe, _Symbol, InpPartialsRsiPeriod, InpPartialsRsiOverBoughtLevel, InpPartialsRsiOverSoldLevel))

return INIT_PARAMETERS_INCORRECT;

// Condition config

ConditionalPartialConfig config;

config.condition = rsi_condition;

config.min_distance_to_close_pos = CreateDiffptr(MODE_DIFF_BY_ATR, _Symbol, g_atr, 0, InpPartialsMinDistanceInAtrMul);

config.str_percentage_volume_to_close = InpPartialsVolumeToClosePercentage;

config.magic_number = InpMagic;

// Init partials

if(!g_partials.Init(config))

return INIT_PARAMETERS_INCORRECT;

else

CAutoCleaner::AddPtr(g_partials); // Añadimos al cleaner

if(InpPartialsClassManagerType == CONDITIONAL_PARTIAL_CLASS_TYPE_CONSTANT)

{

CConditionalPartialsConst* partial = (CConditionalPartialsConst*)g_partials;

partial.ForzeToClose(true);

}

}

Utils

Fibbonaci

CFibbo fibbo;

fibbo.Create(ChartID(), "Fibbo", 0, clrGreen, STYLE_SOLID, 1, "Fibbonaci");

fibbo.SetLevels("0.0,0.2,1.0,2.0", "clrRed,clrRed,clrRed,clrRed", STYLE_SOLID, 1, ',');

fibbo.Move(D'2025.01.01 10:00:00', D'2026.01.01 10:00:00', 1000.0, 1050.0);

double tp = fibbo.GetLevelPrice(2.0);

double sl = fibbo.GetLevelPrice(0.2);

GraphicObjects

RectangleCreate(...);

EventCreate(...);

ArrowRightPriceCreate(..);

.

.

.

// +10 Functions

SetFile

void OnStart()

{

//---

CSetFile sf;

sf.Init("BotSimple");

sf.AddParamLineNumber("InpMagic", 100, 100, 1, 999);

sf.AddParamLineReal("InpRisk", 1.0, 2, 0.1, 0.1, 10.0);

sf.AddParamLineBool("InpUseFilter", false);

sf.AddParamLineDatetime("InpStartDate", D'2024.01.01', D'2020.01.01', 86400, D'2025.12.31');

sf.AddParamLineColor("InpLineColor", clrRed);

sf.ModifyParamValueNumber("InpMagic", 999);

sf.ModifyParamValueRealNumber("InpRisk", 5.5, 2);

sf.ModifyParamValueBoolean("InpUseFilter", true);

sf.ModifyParamValueDatetime("InpStartDate", D'2025.06.01');

sf.ModifyParamValueColor("InpLineColor", clrBlue);

sf.ModifyParamOptDatetimeStart("InpStartDate", D'2023.01.01');

sf.ModifyParamOptDatetimeStep("InpStartDate", 3600);

sf.ModifyParamOptDatetimeStop("InpStartDate", D'2026.01.01');

sf.Imprimir();

}

These are only 5-10% of the classes available in MQLArticles; only the most important classes in the library were represented.

Repository Structure

| Folder | Description |

|---|---|

| Defines | Markdown files containing optional defines to activate or increase logging verbosity for specific classes in the repository. |

| Examples | Basic examples that implement various libraries from the MQLArticles repository, such as risk management, position management, etc. |

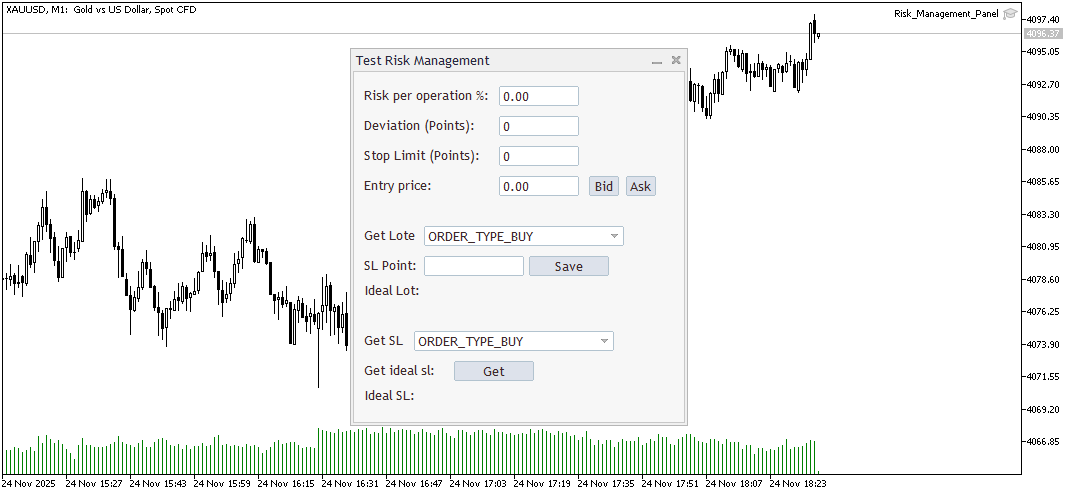

| Images | Screenshots and visual assets from repository examples (breakeven manager, lot size calculator, order blocks indicator). |

| IndicatorsCts | Wrapper library for implementing technical indicators. |

| Ob | Order Blocks indicator implementation and example Expert Advisors from published articles (author: nique_372). |

| PosMgmt | Position management libraries including: - Breakeven management - Partial position closure - Conditional partial closure with indicator-based conditions |

| RM | Complete Risk Management (RM) library modules. |

| Utils | Core utility library for EAs, indicators, and libraries. |

| Sets | Preset configuration files (.set) used in articles published by nique_372. |

| Strategy | Strategy implementation framework for the MQLArticles ecosystem. |

Examples

- Examples\GUI\BE\Ea.mq5

- Examples\GUI\Risk_Management_Panel.mq5

- Ob\Indicator\OrderBlockIndPart2.mq5

Implemented Article Series

Risk Management

| Part | Main Topic | Article Link |

|---|---|---|

| Part 1 | Risk management fundamentals | [EN] |

| Part 2 | Lot size calculation | [ES] |

| Part 3 | Base class construction | [ES] |

| Part 4 | Completing key functions of the CRiskManagement class | [ES] |

| Part 5 | Integrating risk management into an EA (Order Block) | [ES] |

Important Update: The RiskManagement library has been completely renovated since the last publication (part 5).

Position Management - Breakeven

| Part | Focus | Article Link |

|---|---|---|

| Part 1 | Base class and breakeven by fixed points | [ES] |

| Part 2 | Breakeven by ATR and RRR | [ES] |

Position Management - Partial Closes

| Focus | Article Link |

|---|---|

| Implementation of partial closes in MQL5 | [ES] |

Position Management - Conditional partial closure

| Focus | Article Link |

|---|---|

| Implementation of the base class in MQL5 | [ES] |

Order Block Indicator

| Part | Focus | Article Link |

|---|---|---|

| Part 1 | Initial implementation of Order Blocks in an indicator | [EN] |

| Part 2 | Signal implementation in the Order Block indicator | [EN] |

License

By downloading or using this repository, you accept the license terms.

Requirements

See the dependencies.json file.

Installation of repo code

cd "C:\Users\YOUR USER\AppData\Roaming\MetaQuotes\Terminal\YOUR ID\MQL5\Shared Projects"

tsndep install "https://forge.mql5.io/nique_372/MQLArticles.git"

- For use tsndep command requerid tsndep pacakage (avaible in pypi).. This command automatically downloads all dependencies and installs all requirements from the repositories.

- If any part of the system is private, then it will fail... contact me so I can give you access (if it's a product, you can buy it; if you have any questions, don't hesitate to contact me), Check the dependencies.json file for more info.

Contact

- Platform: MQL5 Community

- Profile: https://www.mql5.com/es/users/nique_372

- My Articles https://www.mql5.com/es/users/nique_372/publications